Cleantech startups: German utilities bridging the valley of death?

4 reasons why Cleantech startups failed in the past

Starting a new company in the energy sector, especially in the clean tech branch, is risky and every so often not successful. Still, in the period from 2006-2008 clean tech was one of the hot topics for venture capital funds.

John Doerr, a partner at the prominent Silicon Valley VC firm Kleiner Perkins, announced in a 2007 TED talk that, “Green technologies—going green—is bigger than the internet. It could be the biggest economic opportunity of the 21st century.”

Basically, this enthusiasm about clean tech was driven by high oil prices, which were anticipated to rise further and far beyond 100$/barrel. Today, we know that these expectations were not met.

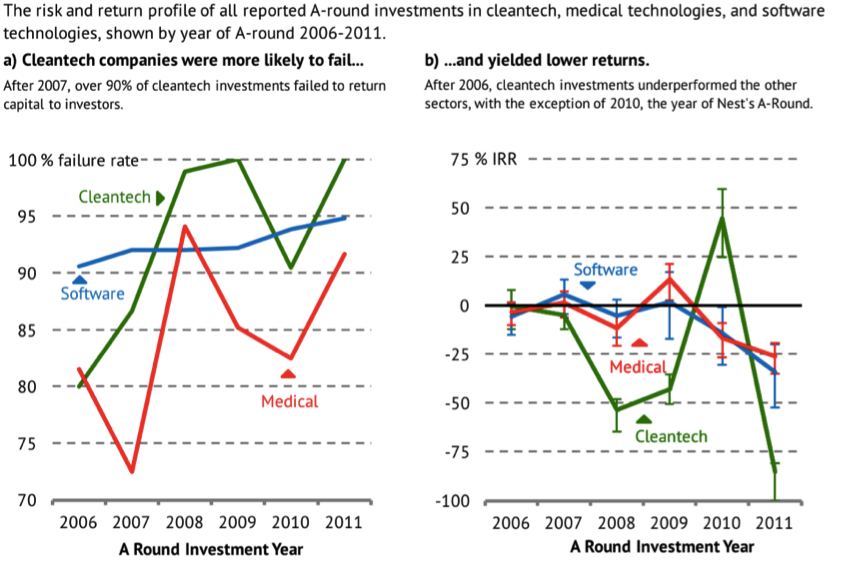

Cleantech startups weren’t able to meet the high expectations either. At the MIT Gaddy et al (2016) compared the data from clean tech with two other technology sectors: Software and Medical. From this data we can learn that cleantech startups performed very poorly compared to startups in the other sectors (even though the two sectors had a comparable environment for startups).

Figure 1: Risk and reward for cleantech investors compared to software and medical technologies (source: Gaddy et al. (2016))

Figure 1 illustrates the relatively high failure rate of clean tech startups as well as the resulting low Internal Rate of Return (IRR). In 2010, Google acquired Nest, which is the only reason why the IRR in 2010 for cleantech is above -25%.

Now, what are the reasons why clean tech startups struggle so much?

Gaddy et al (2016) identify four reasons that help us to understand why cleantech startups perform so badly compared to software and medical startups.

- Cleantech Development needs time (normally longer than the 3-5 years which are expected by venture capital funds)

- Cleantech is expensive to scale as you need large factories even before your product is finalized

- Cleantech focuses on commodity markets with high competition and low margins, which reduces the ability to invest in Research &Development

- Cleantech lags incumbent companies that are willing to take the risk and acquire startups

The first two reasons can explain why clean tech underperforms compared to software startups and why most startups outside the clean tech sector are focusing on digital products or services. But high investment costs for R&D and production are required for the medical sector as well. Here, clean tech loses the comparison because of the last reason mentioned above. While companies in the medical sector have always been willing to invest in startups to bridge the gap between venture capital and mass market, energy utilities were not. Cleantech startups therefore entered the valley of death between prototyping and mass markets. But this is changing.

Utilities investment in startups is increasing

Since 2013, utilities in the US and EU increased their venture capital investments as well as their acquisition activities. While the investments from 2013 and 2014 were considerably higher than in the period from 2010 and 2012, the real action took place in 2015 and 2016, according to the data from GTM Research. This development is summarized in figure 2.

Figure 2: Utiliy Investments in Distributed Energy Companies in the US and EU, 2010-2016 (source: GTM Research, 2017)

Importantly, the reported numbers by GTM Research are probably only a fraction of the real investments, as these are often confidential. Still, figure 2 illustrates quite nicely that utilities expanded their investments in RES-related businesses significantly in the last years. A large share of the most active utilities actually comes from Europe, with two German utilities (E.on & RWE) being among the top 5.

Figure 3: Top Five Utility distributed energy investment portfolios (source: GTM Research 2017)

Due to the energy transition, we can expect that German utilities have a locational advantage when it comes to cleantech investments compared to companies from regions where renewable electricity supply (RES) has less relevance. Lets take a brief look at the situation in Germany and what has changed here.

Three reasons why Germany might become the #1 incubator for cleantech startups

1. Cannibalism Problem of RES solved

Till 2015, German utilities were quite reluctant to invest in RES and in companies whose business case was solely focuses on these technologies. This was mainly due to the fact that an investment in RES would have resulted in the cannibalism of the conventional power generation businesses. In this paper we discuss how the utilities in Germany were challenged by RES and how they tried to adapt to this situation starting in 2015. In a nutshell, the analysis in this paper comes down to this: RES in Germany reduces the average price (-50% between 2008 and 2014) for electricity generation sold via the spot market, which reduces the revenue for conventional power plants. Since 2010, these price reductions reached a level where it becomes difficult for conventional power plants to operate at least on a cost-covering basis. Therefore, an investment by a utility into RES or RES-related businesses would result in a further reduction of revenue from the conventional business, which is why we talk about cannibalism in this context.

In consequence, uutilities therefore focused on their conventional business and hesitated to invest in RES-related businesses. Starting in 2015, the two largest utilities in Germany changed their strategy. E.on as well as RWE split their companies into two independent branches: One company focusing on the conventional generation business (uniper in the case of E.on and RWE) and one company for RES, retail and network operation (E.on and innogy in the case of RWE). With these splits, the cannibalism problem became obsolete: innogy and E.on now don’t have any conventional power plants in their portfolio giving them the freedom to invest in RES and RES-related businesses.

2. Utilities establish new innovation processes

In addition to the change of the organizational structure, both innogy and E.on have applied new innovation processes. While startups and startup-investments did not use to play a huge role in the German utility sector, this has changed to some extent since 2015. Many German utilities have established accelerator programs for energy startups, among them E.on and innogy. While these developments are still in the early beginning, they are one milestone towards a more innovation-oriented energy business.

3. Digitization reduces development time and upfront investments

Parallel to these developments on the investor side, another very fundamental character of cleantech is changing right now: Due to the increasing digitization innovations take less time and money. For details about the digitization, in the German energy sector take a look at our post here.

So far, cleantech has been limited to production or in some cases consumption assets like power generators. Now, with smart metering and other intelligent network assets data becomes available on energy consumption, production and the network infrastructure. Startups can make use of this data to develop new business models. Thereby, innovation moves from technologies with high investments towards less expensive digital applications. We know from the telecommunication sector that a switch from capital-intensive innovation process towards data-driven business models can accelerate the innovation process. Maybe we will see a similar dynamic market development within a digital energy economy as well. For now, we can at least conclude that the on-going digitalization of the energy sector helps to address two key challenges for cleantech startups in the past and two main reasons for the valley of death for cleantech startups: long development time and high upfront investments into production facilities.

Conclusion

Whether these increasing investment activities by utilities together with the first attempts to digitize the energy sector will already be enough to overcome the “valley of death” for cleantech startups cannot be answered from today’s perspective. But at least there is some light on the horizon for the cleantech- & RES-related startup branch.

What are your expectations? Will we see a significant change in the energy related cleantech startup scene in Germany soon? What are the main obstacles from your point of view? Do you have examples that show the changing innovation approach of the German utilities?

Are distribution network operators in Europe threatened by a potential application of blockchain technology in the energy sector? This seems to be the pressing question that was at least partially the motivation for a recent report on blockchain in the energy sector by eurelectric, which is the European association of the distribution grid operators. From our perspective, this report reads like an attempt by the industry to reassure itself that its core business model – asset ownership and operation of the electricity networks – is not threatened by blockchain. While this might be true for asset ownership, this is different in the case of network operation.